|

![]()

| STRATEGIC MANAGEMENT: AN INTEGRATIVE PERSPECTIVE by Arnoldo C. Hax & Nicholas S. Majluf 1 |

| PART 1 |

Planning is an elusive subject. There is no such thing as "an effective unique way to plan". Planning is a complex social activity that cannot be simply structured by rules of thumbs or quantitative procedures. The essence of planning is to organize, in a disciplined way, the major tasks that the firm has to address to maintain an operational efficiency in its existing businesses and to guide the organization into a new and better future.

An effective planning system has to deal with two relevant dimensions: responding to changes in the external environment and creatively deploying internal resources to improve the competitive position of the firm. The maintenance of a vigilant attitude toward external changes is a major driving force behind the capability shown by firms to survive in a hostile environment. The lack of alertness to changes in economic, competitive, social, political, technological, demographic, and legal factors can become extremely detrimental for the sustained growth and profitability of firms.

Planning is the core capacity developed by firms to adapt to environmental movements. This adaptability is not a purely passive response to external forces, but an active, creative, and most decisive search for the conditions that can secure a profitable niche for the firm's businesses.

The internal response of the firm to environmental challenges is given in terms of a clearly defined set of implementable action programs aimed at enhancing the existing and long-term position of the firm vis-a-vis its competitors. Since these action programs define the totality of the major tasks the firm has to face, planning is a most valuable device to coordinate the efforts of the entire organization.

An appropriate planning process must be reflected in adequate functional responses. Manufacturing, distribution, sales, R&D, engineering, personnel, finance, and all functions of the firm should be constantly adapted to respond to new conditions and to achieve increased excellence. But most important still, an effective planning process should be responsive to the individual talents and capabilities that reside in the organization, to the personal aspirations of its members, to the organizational style and corporate values, and to long held beliefs and traditions; in essence, to the organizational culture.

In this part we recognize five major stages in the evolution of planning:

- Budgeting and financial control

- long range planning

- business strategic planning

- corporate strategic planning

- strategic management

A firm does have an appropriate planning system in place when its degree of planning competence matches the degree of complexity of the firm's businesses as well as its internal culture. Each of the above planning stages represents a response to different needs for planning capabilities. Firms do not have the same needs, so it is not surprising to find today many organizations still firmly anchored in the early stages of the planning evolution.

We stated at the beginning that there is no unique way to plan. The type of businesses, the managerial competence, the intensity of competition, the turbulence in the environment, and different cultural conditions call for a planning system coherent with this reality. Moreover, there is more than one way to plan effectively. Rather than looking for the process, business firms should tailor their systems to fit their corporate culture, organizational structure, and administrative processes.

| CHAPTER 1 |

| STAGE 1: BUDGETING AND FINANCIAL CONTROL: |

They emerged more than fifty years ago to maintain within managerial reach the increasing number of activities developed by a firm. Both of them are powerful formal procedures that constitute an integral part of the set of administrative processes used by managers to run a firm and must be intimately related to the formulation and development of strategies in the organization.

| BUDGETING |

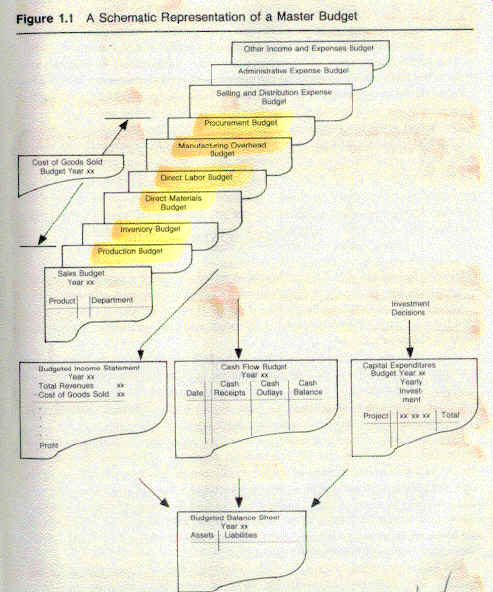

Budgets represent projections of revenues and costs normally covering a one year period. The master budget of a firm includes all those activities whose monitoring is judged to be important for a healthy development of the firm's businesses, among them sales, manufacturing, administrative activities, investment and cash management. Figure 1.1 provides a schematic view of the budgeting process.

A new approach to budgeting calls for the use not only of historical data, but for the establishment of commitments that emerge from a strategic plan, or from negotiations conducted within a Management by Objectives framework [MBO] [Carrol and Tosi 1973].

Thanks to many years of experience with the formulation of budgets, this process has been under continuous refinement and new mechanisms for defining the budget have appeared. For example, flexible budgets permits the original standards being used to measure performance to be modified with the changes in the actual level of operations [Horngren 1982]. Also, Zero base Budgeting [ZBB] establishes a set of very comprehensive rules to force managers to justify their budgetary allocations from ground zero, rather than defining the new budget in an incremental way [Pyhrr 1973 and Stonich 1977].

| FINANCIAL CONTROL |

Originally, financial control was adopted as an administrative system to respond to pressures for better cash management, higher operational efficiency, cost reductions, and constrained financial resources. It provided also a useful mechanism for a decentralized accountability for profit and cost performance at various levels in the organization.

Financial control is a structured process aimed at the efficient and effective use of financial resources, in consonance with corporate strategy.

Financial control measurements are used to judge the performance of the corporation as a whole and of well-defined segments within the corporation. For the latter case, the notion of responsibility center has been developed. Depending on the nature of the management control, it can be defined as an expense center, revenue center, profit center, and investment center.

The financial control system is built around a rather limited number of key variables whose careful monitoring allows managers to track monthly the performance of the various functional activities and business units of the firm. These indicators are derived from the same information used for putting the budget together.

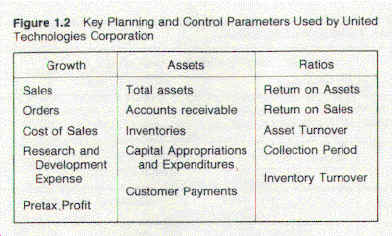

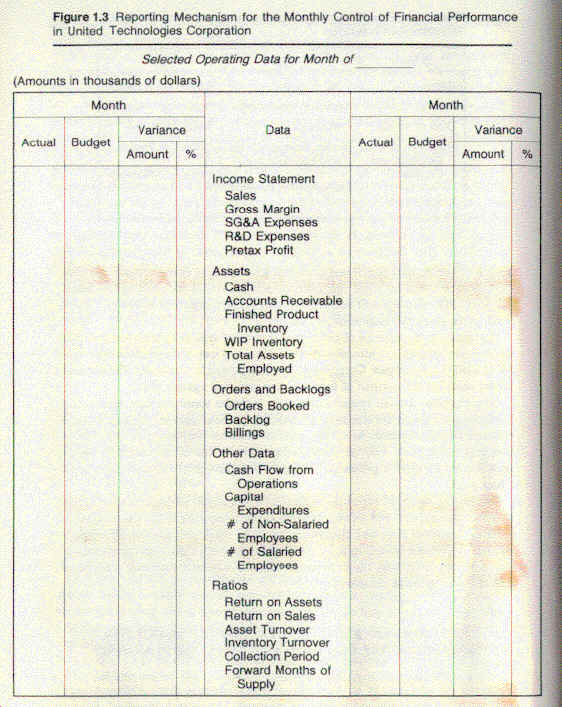

To illustrate the essence of the financial control system in a major American corporation, Figure 1.2 identifies the key planning and control parameters used by United Technologies Corporation; and Figure 1.3 illustrates the monthly report used for the control of financial performance against plan.

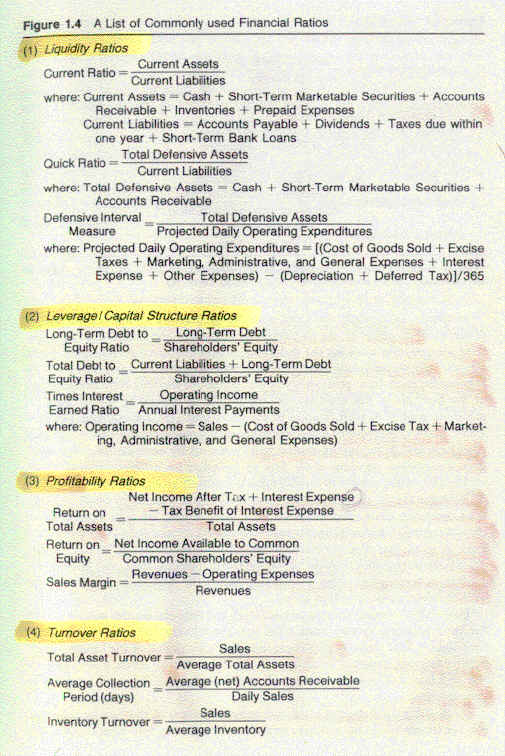

The financial control system commonly includes some absolute measures of performance related to size and growth of the firm operations and a set of selected financial ratios, as in the case of United Technologies Corporation [see Figures 1.2 and 1.3]. A more comprehensive list of the most frequently used financial ratios is presented in Figure 1.4 [Foster 1978]

The use of financial ratios facilitates the comparison of performance among units of different size and among different firms competing in the same industry. With the required financial disclosures imposed upon publicly owned corporations in the United States, ratios have become important standards for competitive comparison. Often, they are used also by external financial analysts as guides for investment decisions.

| THE RELEVANCE AND LIMITATIONS OF BUDGETING AND FINANCIAL CONTROL AS A FORM OF PLANNING |

Financial performance is at the heart of every business firm. Although profit making is not the only objective to be pursued, it cannot be ignored. Lack of profitability will affect adversely all other objectives of the firm.

Figure 1.4 A LIST OF COMMONLY USED FINANCIAL RATIOS

| 1] LIQUIDITY RATIOS: |

Current ratio = Current Assets/current liabilities

where: Current Assets = Cash + Short-Term Marketable Securities + Accounts Receivable + Inventories + Prepaid Expenses

Current Liabilities = Accounts Payable + Dividends + Taxes due within one year + Short-Term Bank Loans

Quick Ratio = Total Defensive Assets/Current liabilities.

Where: Total Defensive Assets = Cash +Short-term Marketable Securities + Accounts Receivable.

Defensive internal measures= Total Defensive Assets/Projected Daily operating expenditures

Where: Projected Daily Operating Expenditures = [(Cost of Goods Sold + Excise Taxes + marketing, Administrative, and General Expenses + Interest Expenses + other Expenses) - (Depreciation + Deferred Tax)]/365

| 2] LEVERAGE/CAPITAL STRUCTURE RATIOS: |

Long-Term Debt to Equity Ratio = Long-Term Debt/Shareholders' Equity

Total Debt to Equity Ratio = Current liabilities + long-Term Debt/Shareholders' Equity

Times Interest Earned Ratio = Operating Income/Annual interest payments

Where: Operating Income = Sales - [Cost of Goods Sold + Excise Tax + Marketing, Administrative, and General Expenses].

| 3] PROFITABILITY RATIOS: |

Return on Total Assets= Net Income After Tax + interest Expense - Tax Benefits of interests expense/Total Assets.

Return on equity= Net income Available to Common/Common Shareholders' equity

Sales Margin = Revenues - Operating Expenses/ Revenues.

| 4] TURNOVER RATIOS: |

Total Asset Turnover= Sales/Average Total Assets

Average Collection Period [days] = Average [net] Accounts Receivable/Daily

Sales.

Inventory Turnover = Sales/ Average Inventory.

OR Inventory Turnover= Cost of Goods Sold/Average Inventory.

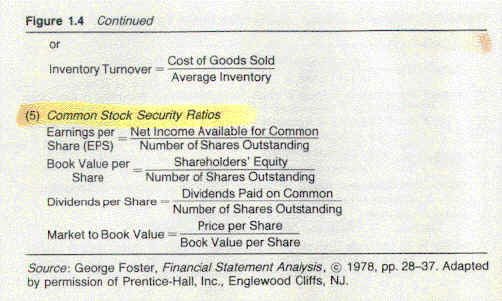

| 5] COMMON STOCK SECURITY RATIOS |

Earnings per Share [EPS]= Net Income Available for Common/Number of Shares Outstanding

Book Value per Share= Shareholders' Equity/Number of Shares Outstanding

Dividends per Share= Dividends Paid on Common/Number of shares outstanding

Market to Book Value = Price per Share/Book value per Share.

Well designed and implemented budgeting and financial control systems are powerful tools for the definition, monitoring, and attainment of profit targets. The major issue, however, is to prevent excessive myopia and undue concern for short-term profitability at the expense of the long-term development of the firm. Much has been said on the pitfalls of depending too strongly on achieving good ROI performances in the short-term [see, for example, Dearden 1969]. Many organizations have found themselves inadvertently weakening their asset base and discouraging necessary investments by compromising the long-term competitive standing of the firm in exchange for a hefty next-year ROI.

The conceptual answer to this dilemma is relatively straightforward, budgeted, ROI figures should stem from the strategic direction selected by the firm rather than becoming goals unto themselves. In other words, strategic commitments should condition financial performance in the short - and long-run. We should keep in mind that a good financial performance is originated by the proper management and development of all physical, technological, and human resources; consequently, rather than manipulating the ROI-index, we should act over the determinants of that index.

Firms which depend entirely on budgetary and financial control measurements for their planning system quite often are exceedingly vulnerable to fall into near-sighted ROI traps. Unless there is a clear articulation of the business competitive strategy, properly understood at all organizational levels, a pure budgeting and financial control system will prove in adequate to avoid undesirable consequences.

Thus, the proper development and communication of the business strategy and the translation of the resulting strategic commitments into meaningful financial indicators are essential requirements to prevent the misuse of budgeting and financial control. One way of assuring this quality of strategy articulation is to adopt a formal strategic planning system. Companies which do not adopt some kind of a formal planning system have to rely on other mechanisms to develop and communicate their strategies, like implicit rather than explicit avenues for strategy formulation, entrepreneurial strategic thinking on the part of the CEO and his top team, and opportunistic decision making. But this planning approach could become increasingly dysfunctional when the complexity of businesses grows. The excessive financial bias would prevent a proper diagnosis of the underlying causes of short - and long-term profitability and would cloud the sense of priorities. Financial targets for a given year can probably be achieved. The main question is, at what price?

| STAGE 2: LONG-RANGE PLANNING |

| THE EMERGENCE OF LONG-RANGE PLANNING |

Substantive progress toward the development of a more comprehensive planning system was made with the introduction of long-range planning in the 1950s. This system called for an organizational-wide effort to define objectives, goals, programs, and budgets over a period of many years.

Long-range planning was a response adopted by many firms to manage more effectively the extraordinary boom triggered during the past World War II period. In order for American firms to respond to this unprecedented growth, it was not enough to rely on a one-year budgetary projection. To meet the required expansions of capacity and to find the corresponding financial resources, it become necessary to extend this planning horizon.

The starting point for long-range planning is a multi-year forecast of the firm's sales. Subsequently, manufacturing, marketing, personnel,and all other functional plans are issued around these initial sales forecasts, which represent a growth commitment on the part of the firm. The final step is the aggregation of the resulting projections into a financial plan that retains the typical measurements of budgeting and financial control, but covering an extended horizon.

The forecasting effort relies heavily on historical projections, typically covering a five-year period. Long-range planning is a bottom-up functional process which generates a set of plans that are little more than budgets extended over a longer time horizon. Perhaps the only additional managerial tool that is introduced with long-range planning is the use of pay-back and discounted cash-flow techniques to evaluate capital expenditures.

![]()

In figure 2-1, we present the form used by a typical American corporation to report its long range plans in 1982. The presentation of historical results facilitates the comparison of observed and forecasted trends.

| LIMITATIONS OF LONG-RANGE PLANNING |

Long-range planning makes sense under the conditions that prevailed after World War II; that is, high market growth, fairly predictable trends, firms with essentially a single dominant business, and relatively low degree of rivalry among competitors.

If the above conditions are not met, long-range planning could become a very frustrating activity. Managers would find time and again that their sales projections would not match actual results and that the tools to diagnose and understand the causes of those deviations would be lacking.

Beginning the planning process with Sales forecasts represents a serious flaw, one should forecast total markets, not sales. The first step in the development of sales projections calls for an analysis of the dynamics exhibited by the market for the various businesses in which the firm is engaged, trying to understand underlying economic, demographic, and attitudinal factors that might be causing its observed behavior. The linkage between total market and sales is market share, which is a decision variable critically important in the definition of the business strategic position. The adoption of a strategic posture can be expressed in terms of market share such as:increase, disinvest, look for a special niche in the market, etc.

The historical projections of sales, so typical of long-range planning, assume that the future will offer a smooth continuity of the past. This is against the very nature of strategic planning, which often leads to drastic discontinuities between the past and the future. Long-range planning can make us fall into the trap of thinking that we are creating a sustained growth situation when, in fact, we are just being driven by highly favorable external forces. When these conditions cease to exist, we are confronted with the difficult task of managing a business in a stagnant economy, which calls for a much more creative form of planning.

Long-range planning does not work under changing external conditions and very intense competitive activities. Likewise, it does not work for a diversified company engaged in a variety of businesses. The functional orientation of long-range planning presupposes a monolithic business structure. When there is a multiplicity of businesses, we have to understand first their inherent differences to provide the support they need for their distinctive development. A bottom-up process will seldom work under these conditions.

Finally, resource allocations in long-range planning are normally done by project, using discounted cash-flow methods. Besides the inability to produce accurate future projections and reliable indicators of financial performance, there is a dangerous loss of strategic vision in approving capital expenditures on a project-by-project basis instead of having a broader view of the long-term implications for the business development. It is relatively easy to evaluate a project in isolation, but it is quite difficult to assess the actual value contributed by a project to a business or a set of businesses of the corporation.

| MERITS OF LONG-RANGE PLANNING |

Though it is unlikely that a firm will face the conditions of environmental stability that would make long-range planning an appropriate strategic process, it constitutes an important first step in the quest for increasing managerial competence.

| CHAPTER 2 |

| STAGE 3: BUSINESS STRATEGIC PLANNING: |

During the 1960s, some important environmental changes began to take place in the United States. The extraordinary growth of the previous period started gradually to temper down, driving up the degree of rivalry among competitors in some of the key American industries. As a result of this process, the focus of managerial attention switched from production to marketing. Previously, every manufactured good could find a place in the market once it was produced; but low industry growth forced firms to pay special attention to the understanding of marketing forces and causes of profitability in order to achieve a defensible position in those areas the firm elected to compete. Moreover, there was an increase in diversification by the most important business firms, often attained via aggressive acquisitions that led in the late 1960s to the third big wave of conglomeration in the United States [Scherer 1980].

| THE EMERGENCE OF BUSINESS SEGMENTATION |

Once the conditions that made possible to successful development of long-range planning ceased to exist, a major new concept emerged creating a most significant development in the practice of planning: the concept of business segmentation. This concept originated in 1970, when Fred Borch, then Chairman of General Electric, decided to break the G.E. business into a set of autonomous units, following a recommendations made by McKinsey and Company. G.E. had evolved from a company restricted to the electrical motors and lighting businesses into a conglomerate of activities spanning a wide variety of industries, Complexity increased as size, diversity, international scope, and a spectrum of technologies began to impose an unprecedented challenge to G.E. top managers. Confronted with this formidable task, G.E.'s answer was to break down the businesses of the firm into independent autonomous units that could be managed as viable and isolated business concern. Those entities were labelled Strategic Business Units, or SBU for short. The SBU concept has produced a long lasting influence in the way companies design, develop, and implement formal strategic planning processes.

A similar notion has been espoused by Arthur D.Little, Inc. [ADL], which defines an SBU as a business area with an external marketplace for goods and services, whose objectives can be established and strategies executed independently of other business areas. It is a unit that could stand alone if divested from the corporation.

ADL's segmentation criteria is based primarily on conditions determined by the external market place rather than production-cost linkages [for example, common manufacturing facilities], technical linkages [for example, common technology], or common distribution channels. They suggest that an SBU is a collection of products and markets that face the same set of competitors, are similarly affected by changes in price, are satisfying a single set of customers, are equally impacted by changes in quality and style, are composed by products which are substitutes of one another, and can be divested without affecting other businesses of the corporation.

The resulting number of SBUs should not be so large as to impair the ability of top managers to understand the broad characteristics of each business and effectively contribute to their proper management. By necessity, therefore, the corporate segmentation in a large firm is rather broad and aggregated.

Normally, the resulting SBUs are thus composed by a plurality of products are markets which have to be properly identified by a secondary segmentation taking place at the business level. This segmentation provides the necessary intelligence for the SBU manager to establish meaningful priorities for the development of each individual segment, including possible abandonment of some of them, in order to concentrate all of the business competencies in a more narrowly focused market.

| THE FUNDAMENTAL ELEMENTS IN FORMAL BUSINESS STRATEGIC PLANNING |

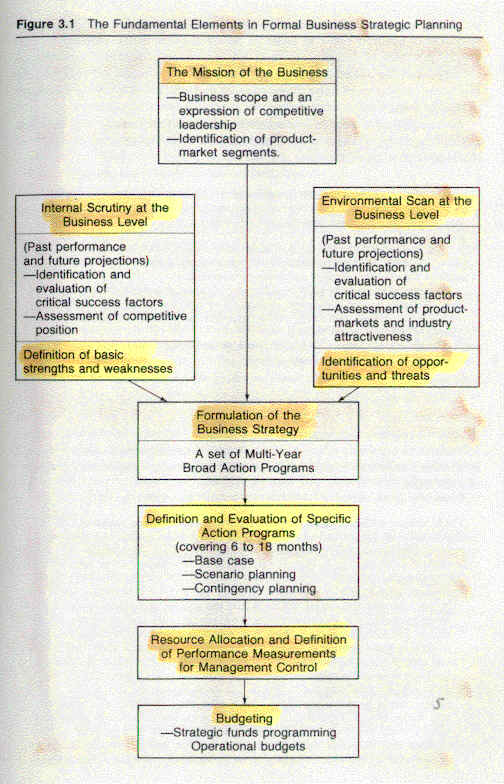

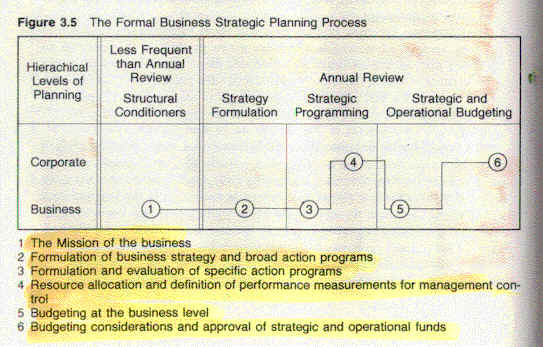

The major tasks to be conducted in a formal business strategic planning process are identified in Figure 3.1. The process is centered in the formulation of the business strategy and their supporting strategic programs. The corporation will evaluate those programs, allocate resources, and make a formal commitment through the agreed-upon budget figures. By adhering to this procedure, the business strategy becomes the end product of a thoughtful process that includes an environmental scan and an internal scrutiny, and requires a previous articulation of the business mission. Now we offer some comments on these steps.

| The Mission of the Business |

An expression of the business purpose, as well as the required degree of excellence to assume a position of competitive leadership,is an essential first step in the formulation of a business strategy. This overall statement of business direction is what we refer to as the mission of the business.

The primary information that should be contained in a statement of mission is a clear definition of current and future expected business scope. This is expressed as a broad description of the products, markets, and geographical coverage of the business today and within a reasonably short time frame, commonly three to five years. The statement of business scope is informative not only for what it includes; it is equally telling for what it leaves out.

The essence of this message is to allow for a broad enough definition of business scope in order to detect changes in the industry trends, the repositioning of competitors in terms of products, markets, geographical coverage, and the availability of new substitutes. The contrast between current and future scope is an effective diagnostic tool to warn against myopic positioning of the business.

The other important piece of information that should be contained in the mission statement of a business is the selection of a way to pursue a position of either leadership or sustainable competitive advantage.

A true leadership position means having a significant and well-defined advantage over all competitors. This can be achieved:

1] Lowest Delivered Cost Position. 2] Differentiated Products.

| Environmental Scan and Internal Scrutiny |

Prior to the development of strategies for the individual businesses, it is necessary to perform a thorough analysis regarding the current and future business position in terms of two dimensions:

- The noncontrollable forces which are associated with the external environment and determine the industry trends and market opportunities; and - The internal competencies residing in the firm, which will determine the unique competitive leadership potential that the firm could mobilize in order to establish a business superiority against competitors.

The business strategy constitutes a response to deal with these two dimensions. When addressing the external environment, the strategic orientation will try to take advantage of market opportunities and neutralize adverse environmental impacts; when facing the internal environment, the direction will be to reinforce internal strengths and improve upon perceived weaknesses with regard to competition.

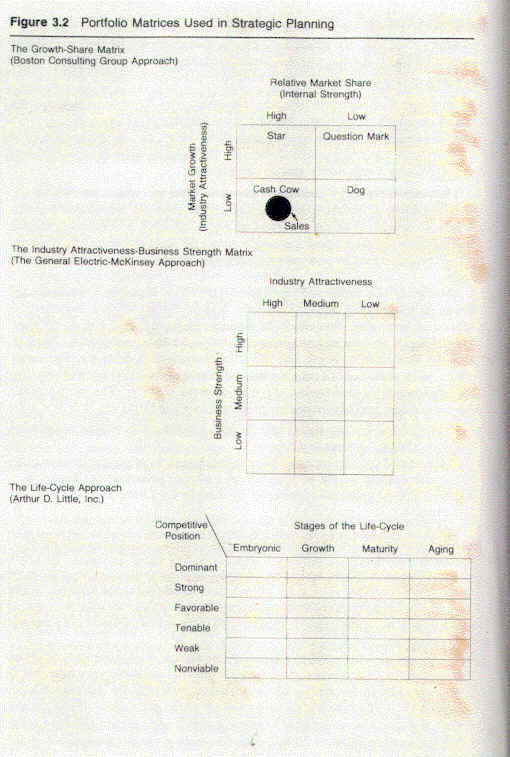

During the late 1960s and throughout the 1970s, a planning methodology known as the business portfolio approach was developed to assist managers in addressing these two dimensions of strategic diagnosis. The essence of these methodologies consists in positioning a business within a matrix in accordance with its competitive strength and the attractiveness of its industry. The result of this effort, presented in a simple graphical display, allows managers to visualize the contribution of each business to the corporate portfolio. The most popular among business portfolio matrices [presented in Figure 3.2] are:

- The growth-share matrix, originally developed by the Boston Consulting Group [BCG], covered in Chapter. 7.

- The industry attractiveness-business strength matrix, originally by General Electric jointly with McKinsey and Co., presented in Chapter 8.

- The life-cycle approach, developed by Arthur D. Little, Inc., discussed in Chapter 9.

Portfolio approaches have made important contributions to the improvement of strategic planning thinking. Some of the most significant among them are: - They represent simple and effective ways to facilitate the decomposition of the firm's activities into a set of well-defined businesses. Moreover, while conducting the necessary analysis to position the businesses in the two-dimensional matrix, ample opportunities exist to reassess the merits of the proposed segmentation.

- By permitting a clear differentiation of the nature of each business in terms of industry attractiveness and competitive position, portfolio approaches allow top managers to set appropriate and distinct strategies for each business in accordance to its inherent potential and development needs.

- Portfolio approaches represent a pragmatic way to capture the essence of strategic analysis. By means of a simple visual display of the portfolio of businesses, they provide a useful device to understand and communicate some important characteristics of the strategic options confronted by the firm.

- Portfolio approaches were most significant in raising the strategic alertness of most managers. To a great extent, the use of portfolio matrices was responsible for accelerating the adoption of formal competitive analyses and for increasing the competitive awareness in American firms. This was accomplished because the implementation of the portfolio approach requires the collection and processing of some minimum quantitative information regarding competitors, which constitutes a useful first step in improving competitive intelligence. Also, portfolio matrices can be easily constructed for major competitors, generating some valuable insights with regard to their overall strengths and some ability to anticipate their potential responses and moves. At the very least, this judgmental call would put in evidence the need to improve the firm's understanding of its major competitors.

- Portfolio approaches have two basic levels of applicability: corporate and business. At the corporate level, they provide the CEO with a useful tool to set up criteria for resource allocation, to reflect upon growth-profitability trade-offs, and to address the question of cash balancing. At the business level, the focus of attention changes from the entire business to product-market segments, but the same portfolio techniques can be used in the process of strategy formulation at a more detailed level.

- Portfolio approaches, by representing the complete collection of businesses of the firm, provide a useful mechanism to consider potential acquisitions and divestitures.

| Formulation of Business Strategies and Definition of Strategic Programs |

The strategic planning process leads to the formulation of the strategy for a business unit. A business strategy is a set of well-coordinated action programs aimed at securing a long-term sustainable competitive advantage. These programs are defined at two different levels of specificity: broad action programs covering a multi-year planning horizon and specific action programs covering a 6 to 18 month period. Therefore, the business strategy is operationally expressed in terms of a series of broad action programs and each one of these is, in turn, explicit as a set of specific action programs. All of these action programs, broad and specific, often involve functional commitments, transforming business strategy in the articulation of properly integrated multifunctional activities.

Perhaps the most significant and permanent contribution of the portfolio approach resides in the generation of a set of natural or generic strategies to be considered by each business depending on their position in the industry attractiveness and competitive strength dimensions. The first proposal of generic strategies came from the BCG approach, which relies on desirable market share positioning as a primary input to convey the strategic objectives for a business unit. The categories of market share thrusts initially defined by BCG ARE: - Increase - Hold -Harvest - Withdraw or Divest. Macmillan [1982] expands the strategic roles which could be played by a business unit depending on its position in the portfolio matrix. Figure 3.3 identifies each strategic role and provides its definition.

FIGURE 3.3: BUSINESS STRATEGIC ROLES EMERGING FROM THE PORTFOLIO APPROACH TO STRATEGIC PLANNING

Build Aggressively: The business is in a strong position in a highly attractive, fast-growing industry and management wants to build share as rapidly as possible. This role is usually assigned to an SBU early in the life cycle, especially when there is little doubt that this rapid growth will be sustained.

Build Gradually: The business is in a strong position in a very attractive, moderate growth industry and management wants to build share, or there is rapid growth but some doubt as to whether this rapid growth will be sustained.

Build Selectively: The business has some good positions in a highly attractive industry and wants to build share where it feels it has strength, or can develop strength, to do so.

Maintain Aggressively: The business is in a strong position in a currently attractive industry and management is determined to aggressively maintain that position.

Maintain selectively: Either the business is in a strong position in an industry that is getting less attractive, or the business is in a moderate position in a highly attractive industry. Management wishes to exploit the situation by maximizing the profitability benefits of selectively serving where it best can do so, but with the minimum additional resource deployments.

Prove Viability: The business is in a less than satisfactory position in a less attractive industry. If the business can provide resources for use elsewhere, management may decide to retain it, but without additional resource support. The onus is on the business to justify retention.

Divest-Liquidate: Neither the business nor the industry has any redeeming features. Barring major exit barriers, the business should be divested.

Competitive Harasser: This is a business with a poor position in either an attractive or highly attractive industry and where competitors with a good position in the industry also compete with the company in other industries.The role competitive harasser is to sporadically or continuously attack the competitor's position, not necessarily with the intention of long-run success. The object is to distract the competition from other areas, deny them from revenue business, or use the business to cross-parry when the competition attacks an important sister business of the strategic aggressor.

Arthur D. Little, Inc. proposes an even further structured and more comprehensive set of generic strategies which are listed in Figure 3.4, and whose use is explored in Chapter 9.

The intent behind the use of generic strategies is not to convert strategic planning in a mechanistic exercise or to reduce the development of strategies to those which naturally coincide with the positioning of the business in the portfolio matrix, but rather to give a menu of reasonable strategic alternatives to the business manager.

The generic strategies can be grouped into six major categories, which emphasize their primary purpose for strategic development.

1] Marketing Strategies: -Export/same product. -Initial market development.- Market penetration. - New Products/New Markets. - New Products/same market. -Same products/New markets. -Same product/same market.

2] Integration Strategies: -Backward Integration - Forward Integration.

3] Go Overseas Strategies: - Development of an Overseas Business. - Development of Overseas Production Facilities. - Licensing Abroad.

4] Logistics Strategies: - Distribution Rationalization. - Excess Capacity. - Market Rationalization. - Production Rationalization. - Product Line Rationalization.

5] Efficiency Strategies: - Methods and Functions Efficiency. - Tecnological Efficiency. - Traditional Cost Cutting Efficiency.

6] Harvest Strategies: - Hesitation - Little Jewel - Pure Survival. - Maintenance. - Unit Abandonment.

FIGURE 3.4 GENERIC STRATEGIES PROPOSED BY ARTHUR D.LITTLE, Backward integration - Development of Overseas business. - Development of overseas facilities - Distribution Rationalization - Excess Capacity. - Export/same product. - Export/same product. -Forward integration. - Hesitation. - Initial Market Development - Licensing Abroad. - Complete Rationalization. -Market Penetration. -Market Rationalization. -Methods and Functions Efficiency - New Products/New Markets. -New product/same market. - Production Rationalization. - Product line rationalization. -Pure survival. - Same Products/new markets. - Same products/same markets. -Technological efficiency. - Traditional Cost Cutting Efficiency. - Unit Abandonment

| Resource Allocation and Definition of Performance Measurements for Management Control |

The ultimate sanctioning of the merits of the business strategy has to reside at the top of the organization where the key resources of the firm are allocated.

Once again, the portfolio approach provides useful guidelines for top managers to address the question of business strategy evaluation and resource allocation.

1] It allows the establishment of an orderly set of priorities for investment, depending on the business potential for growth and profitability derived from its position in the portfolio matrix.

2] It provides a mechanism to check the consistency between business requests of financial and human resources and their inherent needs obtained from their position in the portfolio matrix.

3] It facilitates the proper balancing of cash-requirements and cash-supplies among businesses of the corporation.

4] It permits the establishment control mechanisms suitable for monitoring the performance of each business using key variables consistent with their current and future potential.

| Budgeting |

The result of this planning process leads toward the development of an "intelligent budget", which is not a mere extrapolation of the past into the future, but an instrument that contains both strategic and operational commitments. Strategic commitments pursue the development of new opportunities which very often introduce significant changes in the existing business conditions. Operational commitments, on the other hand, are aimed at the effective maintenance of the existing business base.

A way to break this dichotomy within the budget is to make use of strategic funds and operational funds to distinguish the role that those financial resources will have. Strategic funds are expense items required for the implementation of strategic action programs whose benefits are expected to be accrued in the long-term, beyond the current budget period [Vancil 1972 and Stonich 1980]. Operational funds are those expense items required to maintain the business in its present position.

There are three major components of strategic funds:

1] Investment in tangible assets, such as new production capacity, new machinery and tools, new vehicles for distribution, new office space, new warehouse space, and new acquisitions.

2] Increases [or decreases] in working capital generated from strategic commitments, such as the impact of increases of inventories and receivables resulting from an increase in sale; the need to accumulate larger inventories to provide better services; increasing receivable resulting from a change in the policy of loans to customers, etc.

3] Developmental expenses, that are over and above the needs of existing businesses, such as advertising to introduce a new product or to reposition an existing one; R&D expenses of new products; major cost reduction programs for existing products; introductory discounts, sales promotions, and free samples to stimulate first purchases; development of management systems such as planning,control, and compensation; certain engineering studies, etc.

Although all of them contribute to the same purpose, namely, the improvement of future capabilities of the firm, financial accounting rules treat these three items quite differently. Investment is shown as increase in net assets in the balance sheet and as annual expenses through depreciation in the profit and loss statement. Increases in working capital also enlarge the net assets of the firm, but they have no annual cost repercussion. Developmental expenses are charged as expenses in the current year income statement and have no impact on the balance sheet. Since there are no immediate profitability results derived from these strategic funds, its is important to make a manager accountable for the proper and timely allocation of those expenditures using performance measurements related to the inherent characteristics of the action programs they are attempting to support.

If the business has developed a sound strategy, it will be easy to see how the key performance variables begin to improve with the years. What is more difficult is to measure the short-term contribution of a multitude of programs requiring strategic expenses. Often, it is necessary to resort to project-management type of control mechanisms, centered in cost and time efficiency, as the only way to measure the quality of the implementation of strategic funds.

| THE BUSINESS STRATEGIC PLANNING PROCESS |

A planning process is an organized and discplined way of implementing the sequence of major tasks that are needed for the full development of the business strategy. Figure 3.5 illustrates the nature of that sequence when conducting a business strategic planning process. The six tasks represented in the figure coinside with the fundamental elements described previously. Now we are merely emphasizing the role to be played by the corporate and business levels in the planning process. The corporation limits itself to evaluate business proposals, allocate resources (mostly financial), and provide a final approval for the resulting budget. Since each business unit is supposed to be an autonomous entity having full functional support, the functional participation is implicit at the business level.

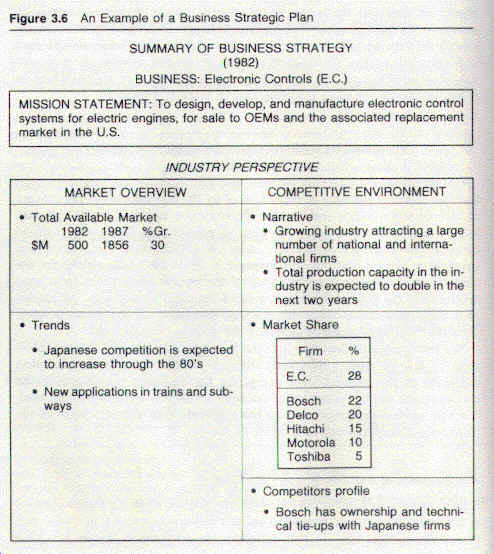

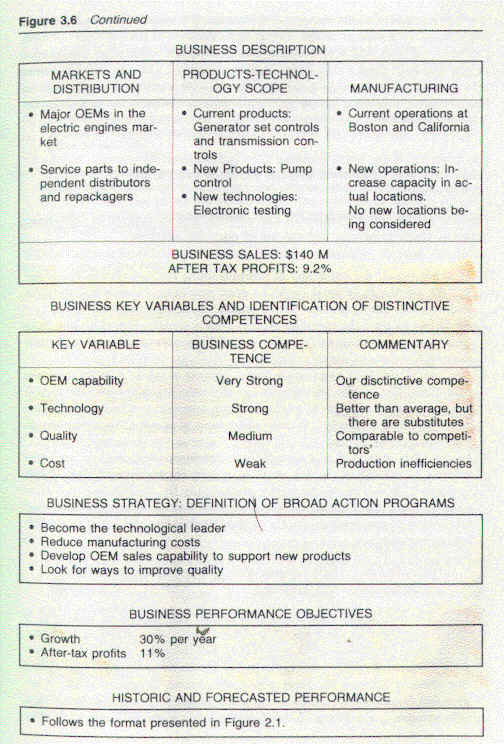

An Example of Formal Business Strategic Planning

| THE CONTRIBUTION OF BUSINESS STRATEGIC PLANNING |

Business strategic planning is characterized by the introduction of the concept of business segmentation and the rise of competitive assessment to the primary level of managerial attention. This form of planning introduces the portfolio approach to address formally the issues of attractiveness and competitive strength. Moreover, the business manager is made fully accountable for the strategic and operational performance of the business and he is given total control over the resources needed to fulfill his managerial duties. All of this constitutes significant accomplishments and represents an extraordinary progress from the long-range planning approach, its historical predecessor.

We have purposely described here the purest form of business strategic planning. By that we mean a situational setting in which there is almost complete autonomy at the business level, except for the necessary sanctioning of the business plans and the allocation of resources to be done at the corporate level. We will address the proper role of the corporation in the next stage of the planning evolution covered in Chapter 4.

| The Relevance of Business Strategic Planning |

This is a legitimate form of strategic planning process whenever the corporation is composed of loosely connected set of unrelated business, as in the case of a conglomerate firm. In that situation, the corporation merely acts as a holding company, monitoring the divisional performance, balancing cash flows, and allocating resources to the competing business activities.

Also, this is an acceptable procedure for a divisional manager in a corporation which has not adopted a more progressive form of planning system. In those circumstances, the divisional manager can move forward creatively in his own area of concern, without waiting for the whole corporation to put its act together. At the same time, this manager could set a constructive example which might inspire other business managers and the corporate officers to improve the quality of the administrative process they have currently in place.

Finally, the evolutionary process that we are describing involves profound educational lessons. Strategic planning requires, more than any other effort, the development of a core management team sharing a sense of values, corporate philosophy, corporate priorities, a deep understanding of the collection of businesses of the firm, and a professional background and managerial competence which will push them to the limits of their creativity. This cannot be acquired overnight, it is the result of a slow process of joint learning through common experiences, which is partly developed by their participation in the formal process of business planning.

| The Limitations of Business Strategic Planning and Further Developments |

There are six important limitations that we could cite with regard to the business strategic planning process and the use of portofolio matrices:

1] By emphasizing the autonomy of business units, the corporation might fail to take advantage of what could be great potentials for sharing resources and concerns among distinct but yet related business activities.

2] By failing to start the planning process with a proper corporate vision, the totality of business plans will not be necessarily convergent toward the betterment of the corporation as a whole.

3] The use of portfolio approaches might become a subtle trap for business executives. The orderly implementation of portfolio analysis and the careful selection of generic strategies might constrain managers to a framework which represses rather than enhances creative thinking, precluding innovation within the firm.

4] In the early stages of the portfolio methodology, there was an excessive reliance in the use of market share as primary measure of competitive strength. This was partly due to the adherence to the experience curve effect [that we present in Chapter 6], which suggests that the firm with the largest accumulated experience enjoys the highest profitability according to the following reasoning:

High Market Share---- High Accumulated Volume-----Lower Unit Cost -------High Profitability.

Exclusive reliance on these arguments creates the impression that there is only one effective way to compete: go after volume and market share. Porter, in his book Competitive Strategies [1980], has presented a convincing argument to cast a doubt on the legitimacy of the above position. He postulates that there is not one but three potentially successful generic strategic approaches to outperform another firm in an industry: overall cost leadership, differentiation, and focus [Figure 3.7].

![]()

5] The traditional portfolio approaches deal with competitive analysis in a fairly informal way. In the book previously referred, Porter [1980] proposes a comprehensive methodology for conducting industry and competitive analysis which has strong relevance to business strategic planning. He identifies five basic forces as determinants of industry profitability which are illustrated in Figure 3.8. An industry will enjoy high and stable profits whenever the firms within that industry can deal effectively with the threats of new entrants and substitutes, neutralize the bargaining power of suppliers and buyers, and establish a moderate to low rivalry among themselves. An explicit description of components affecting each one of these five forces and the way in which they impact the profitability of industry, developed by Management Analysis Center [MAC], is presented in Figure 3.9.

6] The conventional portfolio approaches do not incorporate explicitly the profitability of each individual business unit. It is assumed that a business having a high competitive strength will enjoy a high profitability. Moreover, by providing too much emphasis on cash balancing considerations, a consulting company based in San Francisco, has proposed a different type of portfolio matrix, which they refer to as the profitability matrix, and is discussed in Chapter 10.

After pondering the merits and limitations of business strategic planning, it is an undeniable fact that this stage represents an important step forward in the evolution of planning methodologies. But there is, still, one important question unanswered: What is the proper role to be played by the corporate level in the formulation of business strategy?

( 1 )